Introduction

The nature of blockchain-based applications is decentralization, and their main purpose is to re-launch common financial and non-financial services that use centralization to manage transactions between users. Previously, we dove into two major decentralized finance (DeFi) applications: Stablecoins and Exchanges. We will now turn our attention to yet another significant use of Blockchain: Asset Tokenization.

Asset tokenization can be regarded as one of the next steps in the evolution of transactions. When considering mediums of exchange, we evolved from Limestone [1] transactions to precious metals, commodities-backed paper money, plastic cards, electronic money, and potentially to CBDC in the near future (Central Bank Digital Currencies).

The process of tokenization creates a bridge between real-world assets and their trading, storage and transfer in a digital world. The corresponding process is built by using blockchain technology.

What is asset tokenization?

The tokenization of assets refers to the process of issuing a blockchain digital tradable token [2] that represents ownership rights in a real asset – in many ways similar to the traditional process of securitization, with a modern twist. These security tokens are created through a security token offering (STO), which can produce different tokens such as equity, bond and utility tokens. Security token offerings aim to comply with the security’s regulatory framework at the jurisdiction of issuance and where the offering is marketed.

Tokenized assets can be either directly issued on the blockchain or as conventional securities that are tokenized at a second stage. The latter involves securing the asset in a custodial vault and issuing the digital token to be subsequently traded in secondary markets.

Depending on the source selected, there are many classifications for tokens. The most comprehensive one describes five non-mutually exclusive token categories [3]:

- Platform tokens benefit from the blockchain they are build upon, gaining enhanced security and the ability to support transactional activity;

- Security tokens permit the transfer of ownership;

- Transactional tokens function like traditional currencies, however often with added decentralized benefits;

- Utility tokens are integrated into a blockchain protocol and are used to access the services in that protocol. They have a special quality where the platform provides security for the tokens, and the tokens provide network activity to strengthen the platform’s use and economy; and

- Governance tokens that set the basis for refining the decision-making process, allowing stakeholders to collaborate, debate, and vote on how to manage a system.

The most conventional ones are Utility and Security tokens, and are the subject of this article.

What assets can be tokenized

As a next step, we will analyze what types of assets can be tokenized. Theoretically, any and every asset can be tokenized, but we’ll endeavor to categorize them under a series of concepts.

Tangible v intangible

The primary difference between tangible and intangible is that tangible is something which a person can see, feel or touch and thus they have a physical existence, whereas, the intangible is something which a person cannot see, feel or touch and thus does not have a physical existence. Essentially, tangible assets are characterized by their physical form while intangible are abstract.

Fungible v non-fungible

There are two types of assets that can be represented as blockchain tokens: Fungible assets and non-fungible assets. Fungible assets are interchangeable. An example of this is paper currency, where all same-currency bills hold the same value and are interchangeable. They can also be divisible (dollar into cents for instance).

Non-fungible assets, on the contrary, are unique and not necessarily interchangeable. For example, a real estate asset is typically unique. It is distinguished by its footage, location, materials, etc. No two real estate assets can be equal because they occupy distinct physical spaces. Consequently, they have differing values and they are usually indivisible.

Fungible and non-fungible assets can be represented digitally by a token on blockchain. There are however, theoretically possible combinations via connected smart contracts.

| Fungible | Non-fungible | |

| Tangibles | Paper currency, Precious metals (gold, silver) | Real Estate, Art |

| Intangibles | Digital coins, equity, debt | Patents, licenses, trademarks, Int property |

Table 1: Asset categorization

Main benefits & challenges

Many of the benefits and disadvantages of asset tokenization are inherent to the Blockchain technology they are based upon.

Advantages

- Immutability and transparency. Digital decentralized ledger transactions are an immutable record of ownership, with automatic auditability. A security token has this quality and is capable of having the token holder’s rights and responsibilities embedded. These characteristics promote transparency of transactions, allowing to revise transactional data through enhanced information recording and sharing.

- Universal accessibility. A constant reminder of blockchain benefits is inclusion. Tokenization can leverage the fact that virtually anyone with a smartphone and internet connection can access markets that they previously couldn’t. It can open up investment opportunities to a much wider audience as a result of tokens being infinitely divisible and having lower transaction costs, thus reducing minimum investments and time frames.

- Cost effective. Transaction, liquidation, clearing and settlement processes are optimized on tokenized asset transactions. The use of smart contracts [4] in these processes minimizes the need for intermediaries, hence speeding up transaction times. Furthemore, it cuts the costs incurred through a near-immediate transfer of ownership and updates the continuously reconciling ledger.

- Diversification through fractionalization. Tokenization may allow for the split of assets, dividing ownership into smaller claims. Retail investors, for example, may therefore gain access to asset classes and risks that may have been otherwise beyond their capacity, and can thus participate in capital markets with lower minimum tickets or portfolio sizes. Similarly, access can be gained on investments that weren’t usually available to small retail investors, not because of their high entry costs, but because of their business nature (private equity, for example).

- Compliance. Tokenization can potentially offer new possibilities of automated compliance with regulatory requirements. For example, in jurisdictions applying a limit to the number of investors allowed to participate in an offering, such a limit may be programmed and built into the smart contract used for the distribution of tokenized securities.

- Efficiency. Efficiency gains to be acquired are more important in those markets where there is a high complexity in its process, there are multiple levels of intermediation, speed is low and costs are high, or in markets with a deficiency of trust. As such, a large scale and wider adoption of asset tokenization can be more easily envisaged for private placements of non-listed securities, small-sized bond issuance or private equity/venture capital funds [5].

- Liquidity. The tokenization of assets (especially private securities [6] or illiquid/thinly traded assets like art) permits them to be constantly traded on secondary markets; liquidity increases with improved access to a broader trader base. This benefits investors on both ends by minimizing the illiquidity premium paid.

Challenges

- Securitization. Transparency of collateral, legal clarity of tokenholder claims in relation to underlying assets, protection, pool manager duties, etc. are often critical factors in traditional securitization markets and should be given equal weight in the new tokenization systems.

- Data quality. It should be highlighted, however, that the quality of the data that is inputted into the blockchain is critical for the robustness of information recording and sharing. DLTs do not resolve the ‘garbage in, garbage out’ dilemma; poor data input quality (e.g. malicious or erroneous ‘oracles’ feeding external data into the network) will result in a transparent, immutable, time-stamped repository of unsound or flawed outputs.

- Governance. Governance issues, particularly relevant to fully decentralised ledgers, relate to the difficulty in identifying a sole owner or node accountable for the full network. The absence of a single accountable point is a problem that also arises when regulating DLT networks, or when responsibility for a failure in the network needs to be assigned.

- Trading. Parallel trading of tokenized assets both on-chain and in conventional markets risks creating a bifurcation of markets for the same asset with negative consequences on liquidity conditions and a potential heightened risk of arbitrage [7].

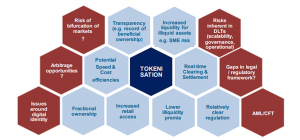

The benefits and challenges of asset tokenization can be summarized in the following chart.

Fig 1: “Benefits and risks of asset tokenization” [8]

Our Tokenization Service

SCALABLE’s Tokenization platform offers our clients the ability to issue cryptocurrencies, security, and utility tokens as well as quickly deploy smart contracts. By tokenizing real estate, commodities, shares, and high-value goods, we channel liquidity where it previously did not exist. With our immutable ledger, diminished costs by issuing native tokens, automated compliance guaranteed by the use of smart contracts, and unmatched liquidity, we provide tokenization that ensures that our customers receive superlative market services. Find out more by booking a demo.

References:

[1] Goldstein, Jacob, and David Kestenbaum. “The Island Of Stone Money.” NPR, NPR, 10 Dec. 2010, www.npr.org/sections/money/2011/02/15/131934618/the-island-of-stone-money?t=1603753241173.

[2] A digital token can be described as a piece of software with a unique asset reference, properties and/or legal rights attached.

[3] “The Different Types of Cryptocurrency Tokens Explained.” Maker Dao Blog, 11 Feb. 2020, blog.makerdao.com/the-different-types-of-cryptocurrency-tokens-explained/.

This is a functional classification. Regulators can use separate categories. The Swiss indirect tax categories, for example, inclue: Asset token, payment token, utility token and hybrid token.

[4] Smart contracts are software algorithms integrated into a blockchain with trigger actions based on predefined parameters

[5] Conversely, public equity markets in developed economies benefit from highly automated and efficient processes where the potential for efficiency gains through the use of DLTs is very limited. Importantly, such markets enjoy high levels of trust by their participants

[6] This does not mean that tokenization of private debt or equity will necessarily overcome asymmetric information issues and difficulty in assessing credit risk related to small companies. Fundamental impediments to the assessment of creditworthiness of SMEs will persist in tokenized markets, although enhanced transparency and availability of data could alleviate part of the information issue, while disintermediation and automation could reduce costs and increase the efficiency of issuing and administering SME securities involving multiple layers of intermediation and a relatively high administrative burden/complexity (e.g. documentation)

[7] Alternatively, it could be argued that if the number of markets an asset trades in increases, the smaller the chances of finding arbitrage opportunities.

[8] SERIES, O. B. P. The Tokenisation of Assets and Potential Implications for Financial Markets. https://www.blockchainwg.eu/wp-content/uploads/2020/03/The-Tokenisation-of-Assets-and-Potential-Implications-for-Financial-Markets.pdf

General Sources:

Laurent, P., T. Chollet, M. Burke, and T. Seers. 2018. “The tokenization of assets is disrupting the financial industry. Are you ready?” Triannual insights from Deloitte. (19). pp.62-67.

Deloitte (2018), The tokenization of assets is disrupting the financial industry. Are you ready? Inside Magazine issue 19, November, https://www2.deloitte.com/lu/en/pages/technology/articles/tokenization-assets-disrupting-financialindustry.html

Forbes (2018), A First For Manhattan: $30M Real Estate Property Tokenized With Blockchain, 3 October, https://www.forbes.com/sites/rachelwolfson/2018/10/03/a-first-for-manhattan-30m-realestate-property-tokenized-with-blockchain/#d3ba39948957